Imagine

standing in a long queue at the bank just to pay an electricity bill or

withdraw a small amount of cash. Hours are wasted, tempers run high, and the

smallest mistake means starting the process all over again. Now picture

completing the same transaction from your phone while sitting at home. No

waiting, no paperwork, and no frustration. That is the power of digital banking.

In today’s world, where time is precious and convenience drives decisions, people often ask: what is digital banking and why does it matter? To understand this, let’s look at the problems traditional banking creates and how digital solutions are reshaping financial life, especially in Bangladesh.

The Problem with Traditional Banking

In

the past, most people in Bangladesh had to walk into a bank branch for every

single service, from deposits to withdrawals. Customers often faced:

Long queues for deposits and

payments

Delays in receiving salary

transfers

Limited branch hours that

clashed with work schedules

Excess paperwork for even basic

services

These

challenges discouraged many from using banks at all. As a result, cash

transactions dominated, which created security risks and slowed down economic

growth. Clearly, a faster and smarter system was needed.

So, What Is Digital Banking?

At

its core, digital banking is

about accessing banking services through technology, so you can manage money

without stepping inside a branch. From opening an account to paying bills,

transferring money, or even applying for loans, everything can be done online

through a website or mobile app.

Think

of it as a bank branch inside your phone or computer. You still access the same

services, but without the hassle of travel and paperwork.

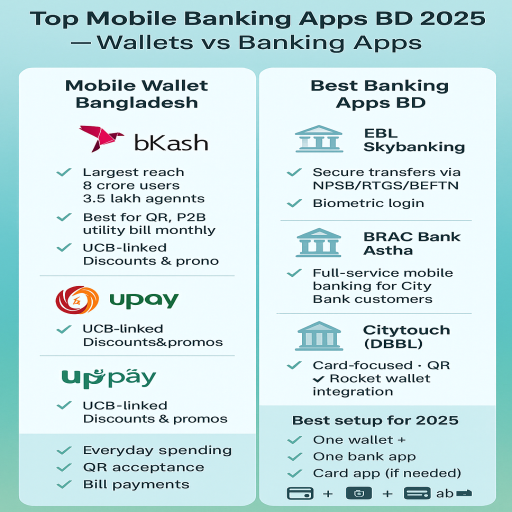

How Digital Banking Works in Bangladesh

In

recent years, Bangladesh has moved forward quickly in adopting financial

technology, making banking easier for millions of people. Almost every major

bank now offers online and mobile services. Dutch-Bangla Bank’s Rocket, BRACBank’s bKash integration, and City Bank’s digital platforms are examples of how

institutions are reshaping customer experience.

Here

is how it applies to everyday life:

This

shift makes life easier for both urban professionals and rural communities who

previously had little or no access to formal banking.

Everyday Benefits of Digital Banking

For

example, a farmer in Rangpur can receive instant payments for his produce

through digital platforms, while a student in Dhaka can recharge their phone

balance online instead of searching for a shop.

Why Digital Banking Matters for Bangladesh

Bangladesh

is moving toward becoming a cashless economy. The government’s Smart

Bangladesh 2041 vision emphasizes technology-driven growth, and digital

finance plays a central role in that journey.

By

adopting digital banking, the

country can:

The

more people adopt digital channels, the closer Bangladesh gets to an economy

that is modern, efficient, and inclusive.

Challenges That Still Exist

While

progress is impressive, there are still obstacles:

However, with growing smartphone usage and government focus on digital literacy, these challenges are gradually being addressed.

The Future of Digital Banking in Bangladesh

As

we move into 2025 and the years that follow, the direction of banking services

is becoming obvious. More banks will expand mobile platforms, artificial

intelligence will enhance customer support, and blockchain may improve

transaction security. Customers can expect personalized financial advice

delivered through apps, seamless international transfers, and even stronger

protection against fraud.

For

individuals, this means banking will continue to become simpler and faster. For

companies, digital systems reduce expenses and allow operations to run more

smoothly.

So,

what is digital banking? In the

simplest terms, it is the ability to access your bank anytime, anywhere, using

technology. It saves time, reduces hassle, and makes financial life smoother.

For

Bangladesh, it is not just about convenience. It is about building a stronger,

more transparent economy where every citizen, from farmers to entrepreneurs,

can participate fully.

If

you still rely on cash or spend hours at a bank branch, maybe it is time to

explore the future. Digital banking puts the branch in your pocket, and the

future of finance in Bangladesh is already here.

FAQs on Digital Banking

Oct 15, 2025

Oct 15, 2025

Oct 06, 2025

Oct 06, 2025

Aug 28, 2025

Aug 28, 2025

Comments (0)

Leave a Comment

No comments yet

Be the first to share your thoughts!